30 Personal Finance Tips That Will Always Be True

Achieving your goals can feel overwhelming at first, but others have trod this road before.

They’ve left behind valuable personal finance tips to help you make it to the next step in your money journey.

No matter which area you choose to focus on first, here are 30 personal finance tips to guide your way.

Budgeting

Ahhh, budgeting. The very first thing we all need to do when we’re getting our money straight, and the very thing most of us are dreading about this whole journey. Budgeting doesn’t have to be awful, though. Just check out these simple tips.

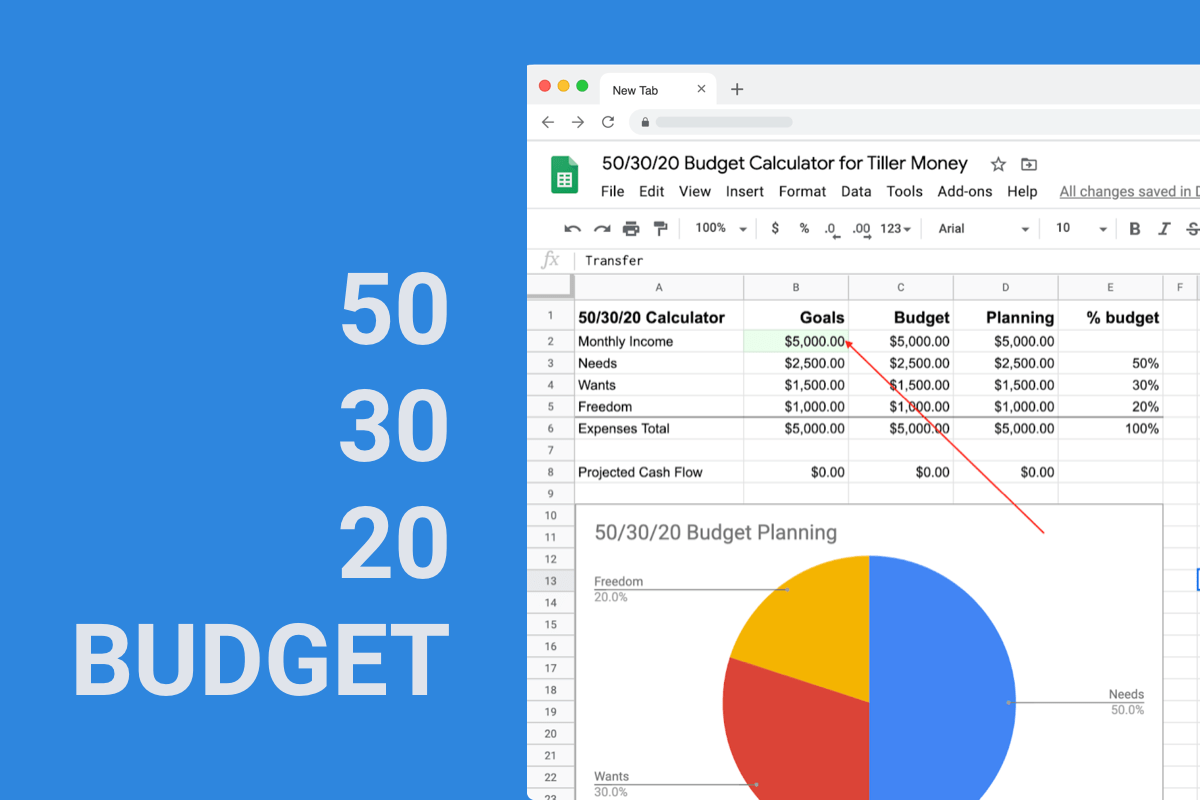

Track your spending.

Back in the day, tracking your spending was an arduous process. You’d have to sift through all your statements, categorizing each purchase.

Luckily, we live in the 21st century, and there are tools like Tiller which can do all that categorization for you.

Examine where you spend your money, and areas where you could cut back. This will give you more money for the things you really value in your budget.

Budget liberally.

Once you’ve got an idea of how much you spend each month and where you’re spending that money, budget liberally. That means budgeting in a little more money than you think you will need in each category. This should set you up for a surplus at the end of the month, or alert you to the fact that you need to pick up a side hustle to meet your expenses.

Being alert to this at the beginning of the month gives you time to fix it by bringing in more money. If you wait until the end of the month, you’ll be a whole lot more stressed out when your till runs dry.

Spend conservatively.

Budgeting liberally isn’t enough in and of itself. In order for that tenant to work properly, you also have to spend conservatively.

That means stopping to think about if each individual purchase lines up with your values. It means looking for deals and clipping coupons.

It means finding every possible way to not spend money. If you budget liberally and spend conservatively, you should have leftover money at the end of each month to throw towards goals like an emergency fund or vacation savings.

Automate your bills.

Remembering 10 due dates per month is exhausting and can result in late fees. Instead of relying on a mental calendar to get the job done, automate this task.

You can either set the bills to come directly out of your checking account on their due dates, or have them paid via a credit card.

If you are able to use credit cards responsibly, you will then only have to remember to pay your card off in full every month on its due date, reducing the number of due dates you need to remember from 10+ down to just one.

Pay yourself first.

When you’re budgeting, it’s easy to put the focus on the money that must be spent rather than the money that should be saved. Flip this, and prioritize the savings first. Put money into your retirement account at work before anything else. Allocate money for your emergency fund before you start budgeting for groceries. As Warren Buffet says, spend what’s left after savings.

Saving for the Everyday

Everyday savings can have a huge impact on your life. It can determine if you’re ready for that next unexpected car repair or if you’re able to attend that friend’s wedding across the country. Look at everyday savings as a form of empowerment and freedom as you implement these rules of thumb.

Build a 3- to 6-month emergency fund. Frankly, a 3- to 6-month emergency fund is going to be considered bare bones in some circles. But having enough money set aside that you know you can pay the bills even without an income for a few months is liberating.

After you’ve hit the 3- to 6-month goal, challenge yourself to see if you can’t build even more financial security by savings up enough to get by for an entire year should something happen to your income.

Don’t finance vacations.

If you want to go on vacation, save for it. Do not put it on a credit card unless you are paying it off in full right away. You may feel that you “deserve” a vacation. We’ll be honest: You probably do. But you’re not doing yourself any favors by putting a trip you can’t afford onto a card you can’t pay off. All you’re doing is making the vacation more expensive as you’ll have to pay crazy high interest rates to get your balance back to zero.

Save regularly for vehicle maintenance.

You’re not alone if you simply hold your breath until the next car repair is needed. But the reality is, vehicles require maintenance. If you own a car or truck, set aside a little money each month for these repairs. When your car finally breaks down or needs new tires, you’ll have the money ready and waiting for you.

If you own your car outright, start paying yourself monthly payments towards a new car. Should your vehicle ever die unexpectedly, you’ll have the cash on hand to buy in your own name rather than borrowing money to finance the purchase.

Don’t spend your windfall.

Encountering a windfall isn’t a regular occurrence, whether it be in the form of a tax refund or an inheritance. It can be really tempting to spend all that money at once, but instead, you should sit on it for a minute.

Think about what you’d like to do with the money, optimizing it to help you reach your financial goals. In the case of particularly large inheritances, it may even be helpful to sit down with a financial professional to evaluate your best options.

After you’ve thought things through, hopefully, the vast majority of your windfall will go towards savings rather than spending.

Automate your savings.

Just as automating your bills ensures they get paid on time, automating your spending can ensure your money routinely ends up in the right account. Set up an automatic transfer with your bank to ensure a set amount of money is getting transferred from your checking account to your savings account(s) every payday.

Investing for your Future

Pensions might as well be a thing of the past, and most millennials don’t count on social security being there for them when they retire. That makes retirement planning more important than it has been since the New Deal was enacted in the 1930s. Let’s dive explore some of the basic rules of thumb.

Just do it.

When you first start investing, it can feel overwhelming. There are all types of ratios to worry about, and you don’t know what the heck asset allocation even means.

The good news is that you don’t necessarily have to know all the vocabulary to get started. The most important keyword in your investing journey will be “compound interest,” and that’s something that needs time to work its magic.

The longer you’re in the market, the more your money has time to grow. If you’re seriously stressed about taking the leap, you may be interested in the simplicity of index fund investing, which is advocated for in JL Collins’ now-famous stock series.

Get that employer match.

If you’re fortunate enough to have an employer who offers a retirement plan and an employer match, take full advantage of the free money.

At the bare minimum, set yourself up so that you’re contributing the max amount your employer will match so you can get to your retirement goals sooner.

Employer plans are often things like 401(k)s or 403(b)s. These accounts are not taxed until you make a withdrawal. That means that the amount you set aside for these accounts will lower your overall income, which lowers the amount of money the federal government can tax you.

If you don’t know if your employer offers a retirement plan or a matching contribution, set up an appointment with your Human Resources department. The free money is worth the little bit of extra effort.

Understand tax implications.

If you have a 401(k) or 403(b), you won’t be taxed upfront. You’ll only be taxed upon withdrawal.

If you don’t have an employer that offers such a plan, you can open a Traditional Individual Retirement Account (IRA) which will operate in the same way. You can also open up a Roth IRA, which is funded with after tax dollars.

Contributing to this type of account won’t lower your overall income for the year, but you won’t have to pay taxes when you start making qualified withdrawals.

Because the money has already been taxed, you can withdraw any of your contributions at any time without penalty. You just won’t be able to withdraw the interest your contributions have earned until you hit retirement age, with a few choice exceptions.

Play the long game.

When you’re investing for retirement, you’re investing for the long haul. Over time, the market has consistently gone up, despite all the peaks and valleys it hits in between.

That means one rough brush with the stock market shouldn’t scare you away for life. Keep investing even through scary economic times, and your long-term plans aren’t likely to be derailed.

Automate your investments.

Noticing a theme here? Automate as much of your finances as you possibly can—including investments. If your retirement plan is through work, you can do this by setting up an appointment with HR. If you have an independent retirement plan, you can set up automatic deposits every pay period through your bank, financial advisor or robo advisor.

Paying off Debt

For many American families, debt is a way of life. It doesn’t have to be, though. If you’ve already dug yourself into a hole, these rules of thumb could help you get your financial life back on track.

Reckon with the numbers.

One of the scariest things about starting your debt payoff journey can be looking at the numbers. They likely aren’t good, but you need to know exactly how much you owe before you can create a strategy to pay it off.

Pick a snow-y method to pay off your debt.

There are two common strategies to paying off debt: The snowball method and the avalanche method.

The avalanche method makes more mathematical sense. You look at all your debts, and start by paying off the one with the highest interest rate.

However, studies have shown that despite it being less mathematically advantageous, those who use the debt snowball method—where one pays off their debts from smallest amounts owed to largest amounts owed—meet with more success.

Allocate specific income towards your debt.

After you’ve meet your monthly expenses, which should include a budgeted amount that goes towards debt payoff, earmark other amounts to be thrown towards debt payment exclusively.

Whether you’re taking the money from your side hustle or simply the surplus leftover from budgeting liberally and spending conservatively every month, the small amounts you throw at your debt will add up more quickly than you’d expect.

Transfer your debt to a 0% interest card.

Many credit card issuers have offers for 0% interest on balance transfers for a set amount of months. This means that instead of paying an APR in the range of 20%-30%, you could significantly reduce your debt by having that number moved down to 0%.

You will still typically have to pay a balance transfer fee, which can range from 3%-5% depending on the company, but most of the time the math adds up to make this method more advantageous than simply leaving your debt on your current card.

You will have to have a positive credit history for the credit card issuer to approve your application, though.

Don’t take on new debt.

As difficult as it may be, don’t take on new debt while you’re paying your current debt off. It can make your numbers really hard to track and your progress difficult to see.

Instead of pulling out the card to swipe, lean on that emergency fund you’ve been building in case of unexpected expenses.

Insuring Yourself

Paying insurance premiums is part of being an adult. If you never have to file a claim, drop to your knees and thank the heavens for your luck.

If you do and you’re not sitting on a pile of cash that would allow you to self-insure, you’ll understand the necessity of them in case you are unfortunate enough to run into catastrophe.

That doesn’t mean you shouldn’t fight to get your premiums as low as you can, though. Here are some basic rules that will help you evaluate risk and cost.

Get a life insurance policy that’s eight to ten times your annual salary.

Heaven forbid something happens to you, you want to make sure your family has the means they need to recover both financially and emotionally.

By getting a policy that’s eight to ten times your annual salary, you’ll be gifting them that time they need to heal. If you have children, you may want to consider adding coverage for their post-secondary education, as well.

Get a renter’s insurance policy.

If you own you have to have homeowners insurance, but no one is going to tell you that renter’s insurance is mandatory—except maybe your landlord. These policies tend to be incredibly cheap, and when they’re bundled with another policy like auto insurance, they may even save you money on your monthly premiums.

Renter’s insurance doesn’t just cover you in case someone gets hurt at your place or the residence burns to the ground in a house fire. It also commonly protects the contents of your car should you get robbed, the contents of your fridge and freezer should you face a power outage and food and shelter should your rental become uninhabitable.

Do the math on your ACA health plan.

ACA premiums are no one’s favorite, but it is nice to live in a world where everyone who wants health insurance can have access to it. This wasn’t the case here in the United States prior to 2014.

When you’re picking out your plan for the coming year, there are a few things you’re going to want to keep in mind as you run the numbers. First, you need to decide how much coverage you need.

If you don’t go to the doctor often and are relatively young, you might decide to take on the risk of a High Deductible Healthcare Plan (HDHP).

The premiums on these accounts are extremely low, and having one allows you to open up a Health Savings Account (HSA) where you can stash money for future healthcare expenses, sheltering it from the IRS. However, when you do need to go to the doctor, you’ll be reminded of what the HD in HDHP stands for.

If you do require routine care, an HDHP isn’t for you. You’ll likely find yourself browsing silver and gold plans on the marketplace.

Bear in mind that subsidies are based on your income, and that full subsidies are based on the cost of a silver plan in your area. From year to year, the gap between gold and silver plan prices varies, which means that those receiving subsidies could conceivably get better coverage for a steal depending on the competition in your area in any given year.

Consider disability insurance.

Disability insurance isn’t as common as life insurance, but it probably should be. According to the Social Security Administration, at age 20, your odds of becoming disabled to a point where you can’t work before traditional social security age are somewhere between 26.8%-28.1%.

Your odds of dying in that same time period—without ever having collected SSI due to disability—are only 5.9%-7.7%.

We’re more likely to run into disability, yet we’re more likely to buy life insurance. If you want to fully protect your family’s income, you can do both.

Ask for discounts.

Insurance companies do offer discounts. For example, your health insurance company might offer some type of refund or gift card if you’re exercising regularly. If you don’t smoke, you can view the lack of a smoking penalty on your life insurance policy as a discount.

Auto insurers give out all kinds of discounts based on all kinds of things: Your job, your age, your marital status, your vehicle’s safety features, etc. Call your insurers today to see if you currently qualify for any of their discounts, or to see if there’s anything you can do to earn them—like hitting the gym.

Because insurance premiums are something you’re bound to pay repeatedly, making one phone call can save you a lot of cumulative cash over the long term.

Reaching Life’s Milestones

Pay for your retirement before their college.

As parents, we have a tendency to want to sacrifice all for our kids. But we need to remember that if we’re not healthy—physically or financially—we’re going to have a lot harder of a time helping our children. In fact, we could turn into a burden on them.

They wouldn’t say it that way, of course, but when you hit traditional retirement age, you’re probably going to be incurring some type of health problem that you do not have right now.

If you don’t have the means to pay for the healthcare you’re going to require, your finances are going to drown fast. So you’ll either be unhealthy or in financial ruin or both, and your child is going to do everything they can to help you—even if it means sacrificing.

You’d both be far better off if you max out all of your retirement accounts every year. If you have money leftover to help them, you should without a doubt help them. But if you don’t have that kind of money, help them through the grant and scholarship process instead.

Your child can run a cost/benefit analysis on school, choosing whether it makes sense to incur debt. You, on the other hand, don’t get to choose to be old and sick someday, and choice few are going to lend you money for that endeavor.

Grants and scholarships are everyone’s best friends.

You and/or your child can go to school even though college is expensive. First, fill out the FAFSA. Even if you don’t get any grants from the FAFSA, it needs to be filled out in order for most schools to offer institutional financial aid packages.

You can also find scholarships throughout your community, throughout the country and even throughout the world.

There is money for education out there.

You or your child simply have to do the work in finding it, and then submit an award-winning essay in most cases. It’s easier than you think, and if you master the essay and make smart fiscal decisions about which college or university to attend, a four-year degree is attainable without incurring debt.

Even if you do incur a little debt (don’t take on too much!) a college degree is still worth it.

The latest Bureau of Labor Statistics Usual Weekly Earnings Report reveals that those with a 4-year degree make an average of more than $500 more per week than those with a high school diploma only, adding up to an additional $26,000 of income per year.

Talk to your partner about money before getting married or moving in together. Talking about money is almost never comfortable, but it’s of the utmost importance to have the conversation with your partner—especially if you’re thinking about getting

Tagged: budget, Financial Journey, milestones, personal finance tips