How the One-Number Budget Keeps You In Control of Your Money

Over in the Tiller Community, a member asked about using the One-Number Budget in a spreadsheet:

“I am trying to create a sheet that functions as a One Number Budget. I have attempted to use the Spending Money sheet, but it doesn’t work as I want it to. My plan is to use the Category tab to divide my expenses into Fixed and Variable categories. I aim to create a list of all my fixed expenses, which will update automatically once they’ve been paid from my account. I also want to include my savings and debt payoff goals in the fixed expense category. Ultimately, I want to have a running total that shows how much discretionary spending I have left each month. Unfortunately, I lack the technical know-how to build this sheet myself.”

Tiller is an excellent tool for following the One Number Budget approach, because it imports data from all your financial accounts into one spreadsheet and features customizable categories, tags, and groups.

What is the One-Number Budget?

The One-Number Budget simplifies the process of managing your money by focusing on one key number – your weekly spending limit. This differs from other budgeting methods that require detailed tracking of every expense.

The basic formula is:

Fixed monthly expenses + Average non-monthly expenses + Financial goals – Total monthly income ÷ 4.3 = Your total weekly One-Budget Number for discretionary spending

You can estimate your One-Number Budget with this simple spreadsheet calculator.

Benefits of the One Number Budget Approach

The One-Number Budget has several benefits, especially for those new to budgeting or looking for an easier way to manage their money:

- One clear number avoids confusion with traditional budgeting methods.

- You can easily adjust your spending habits without having to constantly track multiple categories or budgets.

- You always have enough to cover your monthly fixed expenses.

- You’re better prepared for unexpected expenses

“The reason this approach works so well for so many people is because it’s super straightforward — the idea is to calculate how much money you can afford to spend on “flexible costs” (aka the things that you have to make decisions about) each week, and then you only have to remember that one number on a day-to-day basis.” – Sofia Figueroa

Ellevest

Note: for a similar “one number” approach, check out the Monthly Budget Calendar template for Google Sheets and Excel.

How to create a One-Number Budget

1. Gather several months of your finances into one dashboard

Before you can determine your One Number Budget, you’ll need to know your past spending and income trends.

If you’re already using Tiller, your spending and income is already organized in your Google or Excel spreadsheets. If you’re not using Tiller, you can sign up for a free 30-day trial and import up to 3 months (sometimes more) of your past transactions. This makes building your budget much faster and easier. You can cancel your Tiller trial before it ends without being charged.

Alternatively, you can manually import bank CSV files into a Google Spreadsheet.

2. Total your take-home monthly income

Start by adding up all of your monthly take-home income (after taxes and withholdings) into a single number. This should include:

- Your paycheck, salary, or wages

- Any freelance or side hustle income

- All other sources of revenue such as investment dividends.

If you have irregular income or receive payments at different times throughout the year, consider taking an average of your income over the past few months to get an estimate.

💡 Tiller Tip: You can categorize all of your monthly income into a single category or category group. Alternatively, if you track multiple categories of income and don’t want to create an income group, you could tag all income with a single “income” tag.

3. Total your fixed monthly expenses

Fixed monthly expenses reoccur each month and are typically the same amount. For example:

- Rent or mortgage payments

- Annual subscriptions

- Utility bills

- Loan payments

- Insurance

- Minimum debt payments

Add these up, then divide this number by 12 so that you can allocate a monthly amount to these expenses.

Tiller Tip: The Category Tracker Report for Google Sheets or Microsoft Excel can help you drill into your expenses and see totals by month or another custom period.

3. Total your non-monthly expenses

Non-monthly expenses are irregular or infrequent expenses that do not occur on a monthly basis. They might vary in amount and frequency, but still need to be taken into account when creating a budget. Examples include:

- Insurance premiums, such as car or homeowners insurance

- Vehicle maintenance and repairs

- Holiday and birthday gifts

- Medical and dental expenses

- Home maintenance and repairs

Total these expenses and divide by 12 to determine how much to budget each month so you have funds ready when you need them.

4. Total your savings, investment, and debt payoff goals

Determine your financial goals, such as saving for emergencies, buying a house, retirement, and debt payoff.

Keep them realistic and allocate a specific amount of money to each goal.

5. Calculate your One-Number Budget

- Total your monthly fixed expenses, non-fixed expenses, and financial goals together

- Subtract that number from your take-home monthly income

- Divide this number by 4.3 (the average number of weeks in a year) and you have your One Number Budget

Your One-Number budget is the amount you have available each week to spend on discretionary expenses. To be clear, some of these “discretionary” expenses are actually things you need, like:

- Groceries

- Transportation

- Clothing

- Personal care

And some will be optional, like:

- Dining out

- Entertainment

- Hobbies

- Travel

Using your One-Number Budget

Throughout the month, use your One Number to guide your discretionary spending on things like groceries, dining out, entertainment, and shopping. As long as you stay within the limit of your One Number, you’ll be able to cover your fixed expenses and reach your savings and investment goals.

Review and refine along the way

One-Number Budgeting can be a highly effective way to control your finances. However, to make this budgeting strategy successful, it’s important to track your spending and adjust your budget accordingly.

In fact, refining your budget along the way is key to One-Number Budgeting success. This means looking for areas where you can cut back on expenses without sacrificing too much and being flexible and willing to make changes as needed to ensure that your budget remains manageable over time.

The key is to be mindful of your spending and make informed decisions that align with your overall financial plan.

Tips on adapting a Tiller Foundation Template to the One-Number Budget

While the Tiller Community has not yet built a One-Number Budget, there are a couple of ways to customize you category names, groups, and tags in your Tiller Foundation Template to get close.

💡 Tiller Tip: If you want to experiment with changing your categories, we recommend doing so in a copy of your existing spreadsheet.

Creating specific category names to follow the One-Number system will probably get messy fast. Instead, consider using groups that follow the system of fixed monthly expense, non-monthly expense, financial goal, and discretionary expenses:

You can then run a report with the Category Tracker for Google Sheets or Microsoft Excel, to easily see what you’ve spent in each group by week, month, and year.

Or, you can make quick pivot table or create a category filter.

If you don’t want to customize your category groups in this way, you could also use tags:

You can generate a report on tags with the Category Tracker for Google Sheets or Microsoft Excel. For Google Sheets you can also use the Tag Report.

The One-Number Budget vs 50/30/20 Budget

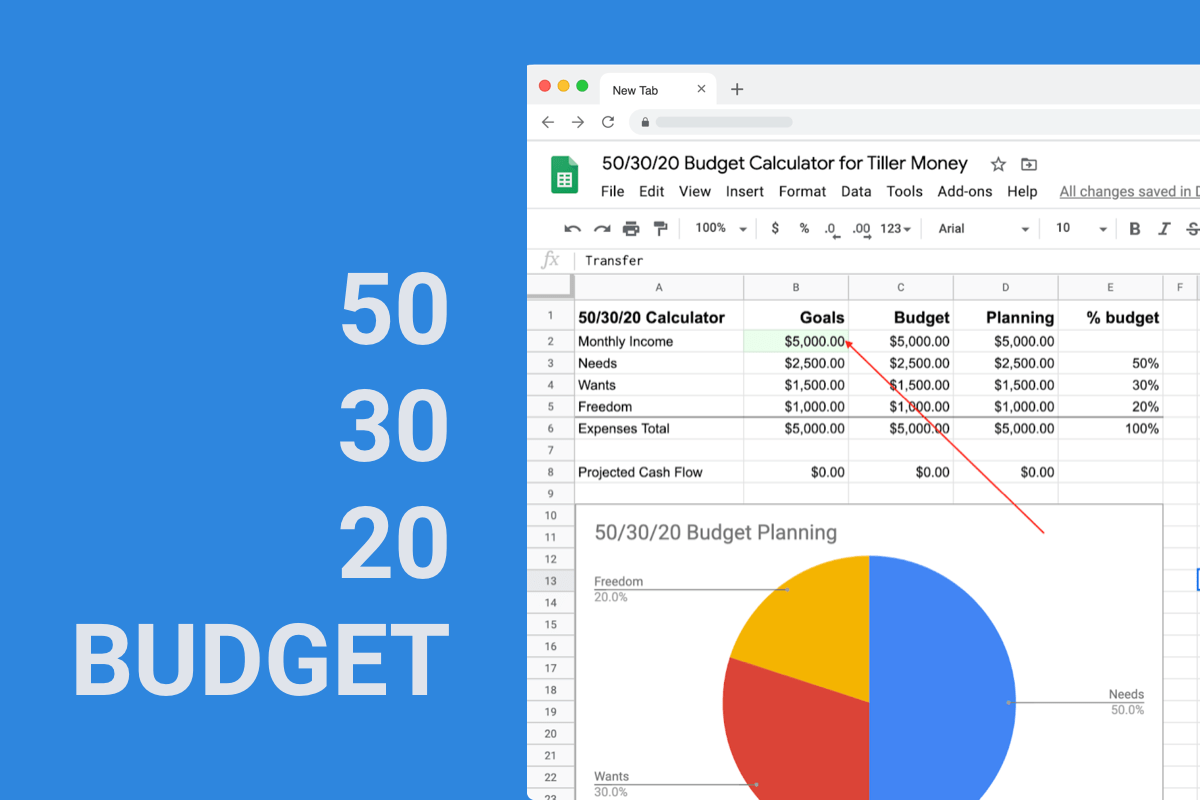

The 50/30/20 budget is a more structured approach to budgeting, which allocates percentages of your take-home pay to three main categories:

- 50% for Needs: This includes essential expenses like housing, utilities, groceries, insurance, and minimum debt payments.

- 30% for Wants: This category covers discretionary spending, such as dining out, entertainment, shopping, and hobbies.

- 20% for Savings and Debt Repayment: This portion is dedicated to building an emergency fund, saving for retirement, paying off debt, or working towards other financial goals.

The main difference between these two budgeting methods is the level of detail and structure. The One-Number Budget simplifies the process to a single spending limit, making it easier to follow and allowing for more flexibility in spending.

The 50/30/20 Budget offers a more detailed framework, providing guidance on how to allocate your income to different categories, which can help ensure a more balanced approach to financial planning. Ultimately, the choice between these budgeting methods depends on personal preferences and financial goals.

Read: The Top 5 Recommended Budgeting Strategies

Who created the One Number Budget?

Financial advisor John W. Crane created the One Number Budget. He wrote the popular, highly rated book “The One-Number Budget: Why Traditional Budgets Fail and What to Do About It”

Click here to read and listen to a great interview with John W. Crane about why he created the One Number Budget.

Edward Shepard

Continue the discussion at community.tillerhq.com

12 more replies

Interesting. I hadn’t heard of a One Number Budget before.

I don’t think I have seen something that has all these pieces organized the exact way you lay out but you can likely find a number of pieces that are close if you search in the Show & Tell section(s). You may be able to pull them together into a single view or just use them as standalone functional sheets.

The new Monthly Budget Calendar might be helpful with seeing “how much discretionary spending I have left each month”.

Thank you for asking this question – I’d never heard of the One Number Budget approach before now! I researched this method and wrote a post about it to share with the rest of the Tiller Community.

If you don’t mind me asking, how did you find the One Number Budget, and why do you like it?

If you simply want to see a running total of your spending vs a target, I agree with Randy that the Monthly Calendar is an easy, customizable way to do this. You could enter your “One number” as your budget target:

I’m hoping someone in the Community builds a dedicated template based on the One Number Budget. In the meantime, there are a couple of ways to customize you category names, groups, and tags in your Tiller Foundation Template to get close.

Note: if you want to experiment with changing your categories, we recommend copying your original spreadsheet and trying your changes there. AutoCat can easily reassign transactions to your new categories, tags, etc.

Creating specific category names to follow the One-Number system will probably get messy fast. Instead, consider using groups that follow the system of fixed monthly expense, non-monthly expense, financial goal, and discretionary expenses:

You can then run a report on your groups with the Category Tracker for Google Sheets or Microsoft Excel, to easily see what you’ve spent in each group by week, month, and year.

Or, you can make quick pivot table or create a category filter.

If you don’t want to customize your category groups in this way, you could also use tags:

You can generate a report on tags with the Category Tracker for Google Sheets or Microsoft Excel. For Google Sheets you can also use the Tag Report.

@Cosmos I am very interested in this budget approach. Conceptually, getting a real-time view of your spending limits makes a lot of sense. I also like how it removes some of the barriers and complexities of traditional budget strategies. Similar to you, I am not technical enough to build the template. I would happily pay someone to make it if they are interested.

@Edward You mentioned copying the sheet to test the method. Just to clarify, are you suggesting duplicating the file in Google Drive and setting up the One Number Budget?

Thanks everyone for your feedback!

@randy Thanks for sharing the new Monthly Budget Calendar! That accomplishes most of what I was looking for. Very cool.

@Edward I only recently learned the solution I have personally used manually had a name. I’ve been looking for an app that would automate a solution like this for a very long time. I finally decided to ask here since this is what I use for managing my personal finances.

As an accounting and finance professional, I am a big believer in budgets for businesses. However, a lot of people (myself included!) don’t have the time or desire to track spending at a granular level. I budget my fixed expenses and savings and debt goals which leaves me with a single number for discretionary spending.

I made adjustments to the Spending Money sheet similar to what you’ve detailed above that allows me to see a remaining balance, but the Monthly Budget Calendar is much cleaner!

My understanding of @Edward’s note about copying the spreadsheet, @EdwardDarrah, was that you could make a copy for experimentation before implementing changes in your master data set.

You could also make the changes in your master and then revert the changes using Google Sheets’ restore functionality if you are not happy with the new approach.