7 Best Budgeting Tips for the New Year

Whether you want to invest more, pay off debt or save up for that sick vacation, there’s one thing you’ll have to master first: The budget.

There are a slew of different budgeting methods. After you pick one that’s right for you, be sure to implement these seven best budgeting tips. Your money will thank you.

- 1 – Negotiate recurring bills.

- 2 – Automate your finances

- 3 – Take advantage of technology

- 4 – Budget liberally. Spend conservatively.

- 5 – Use the debt snowball method rather than the debt avalanche method.

- 6 – Spend money on time, not things

- 7 – I know I’m not going to follow through with my budget. Why bother?

- The answer is simple: Awareness

1 – Negotiate recurring bills.

It may seem like budgeting 101, but we’re willing to bet you haven’t gone in and negotiated your bills in a while, even if you did so when you first moved in. Be sure to call your service providers, insurance providers and anyone else to whom you pay a monthly bill:

- Rent, though you’ll have to negotiate this at the beginning of your contract or at renewal.

- Auto insurance.

- Renter’s/Homeowners insurance.

- Cable.

- Cell phone.

- Utilities.

Be sure to brush up your negotiation skills before you pick up the phone.

2 – Automate your finances

Your bills are due seven times per month. Remembering to pay each one — and to set some money aside for retirement and your emergency fund — can be a lot.

Rather than putting the onus on yourself to remember each and everyone, you can set up automatic payments. You won’t miss any bills, and you’ll know which days to expect the withdrawals.

You can also use automatic transfers to fund any retirement account you have outside of your employer, and build up your 3- to 6-month emergency fund. When savings are automatic, it’s more likely to happen.

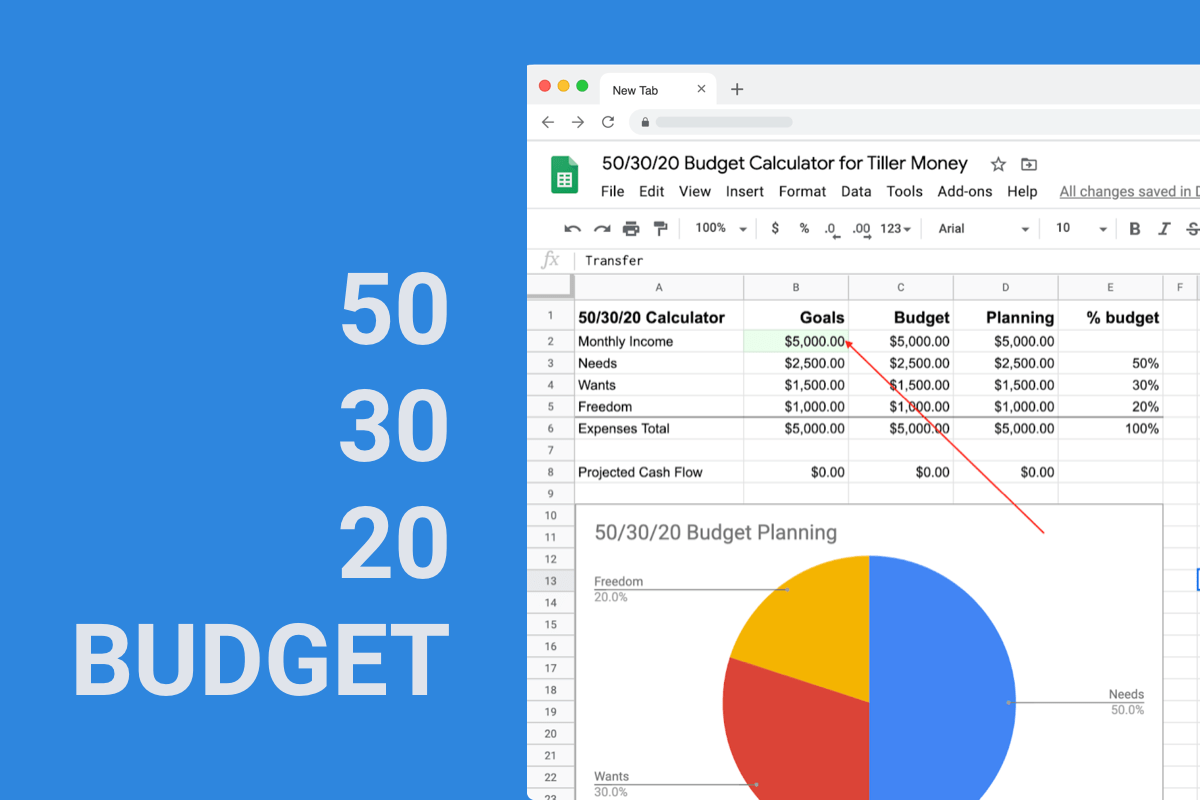

3 – Take advantage of technology

As you automate your finances, take advantage of technology. There are a ton of apps out there that automatically keep track of the money coming into and leaving your accounts.

For example, here at Tiller, we not only track your deposits and withdrawals we also categorize them and provide you with reports that can help you gauge your progress towards your financial goals.

Check out some of the top tech tools to help you keep on top of your money here.

4 – Budget liberally. Spend conservatively.

As you build your budget, keep the golden rule of budgeting in mind: Budget liberally. Spend conservatively.

Budget liberally. Spend conservatively.

What that means is that you’ll want to budget more money than you think you’ll spend. If you think you need $100 for gas, bump it up to $150 just in case. If you think the electric bill will be around $120 as that’s usually the amount you’re charged, budget in $130.

Hopefully you won’t need this extra budget, but if you get hit with extra fees on your electric bill or find yourself driving across the county for an unexpected birthday party for your kids, you’ll have that extra cash on hand rather than scrambling for it.

After you’ve budgeting liberally, be sure to spend conservatively. Use coupons. Take advantage of sales. Live frugally and don’t buy more than you need.

If you’ve written a realistic and liberal budget, these tactics should help you have a surplus rather than a shortage at the end of the month. Feel free to use anything leftover as a slush fund, throw it at your retirement fund or use it to build your emergency fund.

5 – Use the debt snowball method rather than the debt avalanche method.

The debt avalanche method is the most mathematically advantageous way to pay off debt. To use this method, you look at the interest rates on all of your debts.

Make minimum payments on all of them, but throw any extra money you have at the debt with the highest interest rate. When that highest-interest rate debt is paid off, apply all the money you were throwing at it to the debt with the next highest interest rate.

The debt avalanche method may be the best method when we look at the numbers, but when we factor human behavior into the equation, we actually find that the debt snowball method is better.

To use this method, you will list out your debts and rank them according to the total dollar amount you owe. You will pay the smallest debt off first, then throw all your money at the second smallest, then the third, etc.

This method works better in practice presumably because we as human beings like quick wins – even if they end up costing us more money in the long-run. Keep this in mind as you include any debt payoff in your budget.

6 – Spend money on time, not things

A key part of any budget is establishing your priorities and goals. As you write out your goals for the New Year, take note that science tells us we’ll be happier when we spend money on time rather than things.

This doesn’t just mean actually claiming all those PTO hours and prioritizing a vacation over an iPhone.

It also means that we’re happier when we use our money to claim some of our time back from chores and other mundane tasks.

Examples include paying for someone to clean your house, paying that neighborhood kid to take care of your lawn during the summer and taking advantage of curbside services at the grocery store.

7 – I know I’m not going to follow through with my budget. Why bother?

Balancing your figurative checkbook in a world where wage stagnation and income inequality are real and tangible problems can be frustrating at best.

It can be easy to adopt an attitude of despair about your finances: If you’re never going to get ahead, why bother with a task you don’t like doing in the first place?

The answer is simple: Awareness

When we’re more aware of what’s going on with our money, we’re actually happier. This might seem counterintuitive if your money’s a mess. But knowing just how bad of a mess it is can help you feel more empowered to do something about it – at least more empowered than if you were sitting in the dark.

So even if you don’t think you’ll follow your budget to a T, even if you think you’re a shopaholic, even if you think you’ll never, ever get out of debt – set a budget.

Explore the Tiller Foundation Budget to see where you are with your money today.